India is a diverse and populous country and the importance of ensuring the well-being of one’s family cannot be understated. With the rising cost of medical treatment, family health insurance has become a necessity in India, offering protection against escalating medical expenses. According to a recent report published in livemint.com, over 40 crore people in India still lack access to any form of health insurance, highlighting the urgent need for widespread coverage. It is a matter of concern that the number is so high despite the growing awareness in our country.

When selecting a health insurance plan for your family, it is essential to carefully consider factors such as -

Coverage options

Premium costs

Out-of-pocket expenses

Assessing the network of healthcare providers

Additional benefits or perks offered by the plan

By thoroughly evaluating these aspects, you can make an informed decision and choose a health insurance plan that best suits your family’s requirements.

What is the Definition of Family Health Insurance?

A Family Health Insurance plan is a comprehensive way to ensure that your entire family has access to necessary medical care. With this type of plan, you can provide coverage for hospitalization, routine preventive care and more for your loved ones. This can provide a sense of security, knowing that your family’s major healthcare needs can be addressed without causing financial strain.

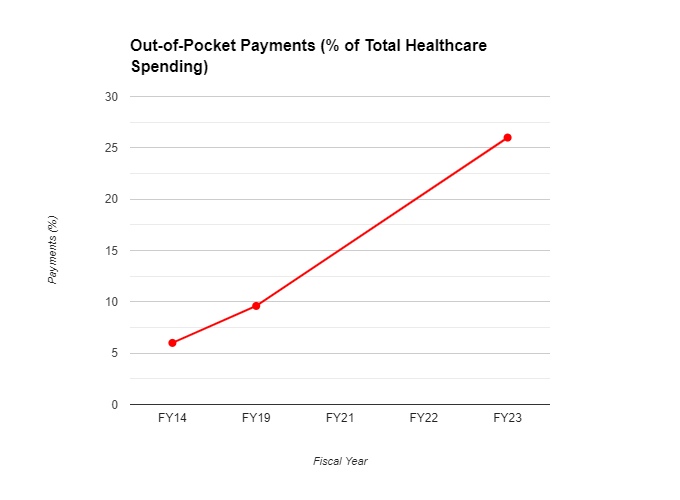

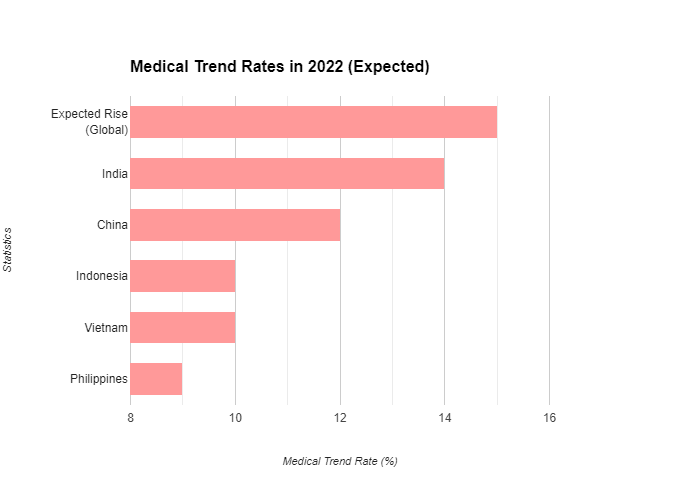

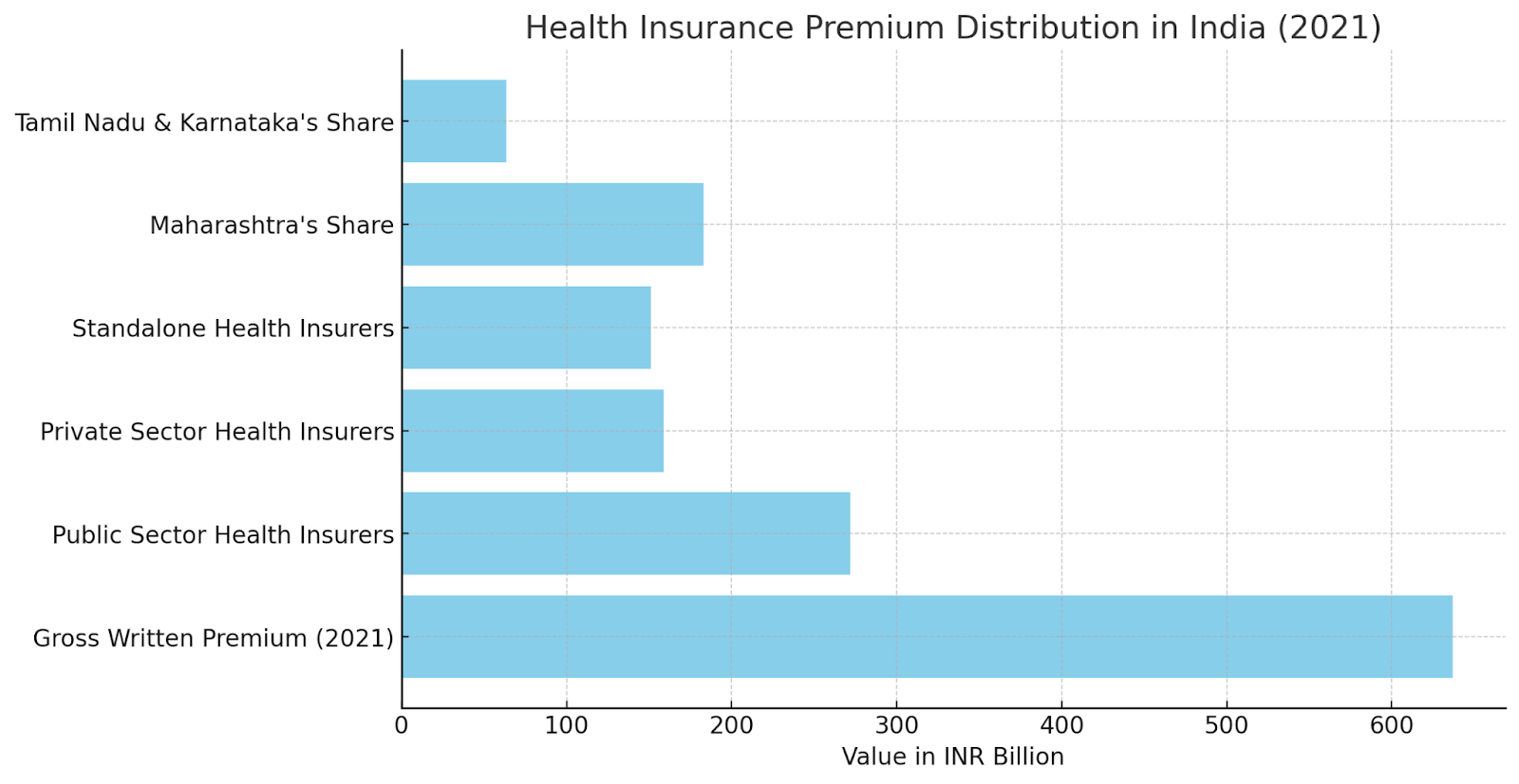

Health Insurance Statistics of India in 2024 (Till July)

Here is a snapshot of the Indian health insurance sector in a statistical format:

Gross Premium Collection of Health Insurance (INR Crores)

Health Insurance Statistics by State

List of Top Family Health Insurance Plans in India in 2025

The table provides an overview of the best family health insurance plans in India for 2025. It includes important information like coverage benefits, network hospitals, maximum sum assured and entry age criteria. These plans are designed to meet diverse healthcare needs, offering a range of features to suit various situations. Families can easily select a suitable option based on their requirements.

What are the Key Components of a Family Health Insurance Plan?

Key components of family health insurance plans often include coverage for medical services such as -

Coverage for Hospitalization Expenses - Provides coverage for a wide range of hospitalization expenses, such as room rent, ICU charges, surgeon’s fees, anaesthesia, blood, oxygen and operation theatre charges, ensuring that the financial burden of medical treatment is eased for the insured individual and their family members.

Pre and Post-Hospitalization Coverage - Many family insurance plans offer coverage for pre-hospitalization expenses, typically for up to 60 days before hospitalization, as well as coverage for post-hospitalization expenses for up to 180 days after discharge.

Daycare Procedures - They often cover daycare procedures that do not require an overnight stay in the hospital, including cataract surgery, dialysis, chemotherapy and other similar procedures. This coverage can be extremely beneficial for individuals who need these treatments but do not need to be hospitalized for an extended time.

Ambulance Charges - They usually provide coverage for ambulance fees in the event of an emergency, ensuring that the insured individual is transported to the hospital without incurring any additional expenses.

Domiciliary Hospitalization - Certain family health insurance plans offer coverage for medical expenses related to treatment at home, in instances where hospitalization is not feasible, known as domiciliary hospitalization. This can be particularly beneficial for patients who require ongoing care and monitoring but do not necessarily need to be admitted to a hospital for treatment.

Cumulative Bonus - Insurers often provide a cumulative bonus that gradually boosts the sum insured with each consecutive year of no claims made. This bonus typically has a limit to how much it can increase.

Cashless Treatment - These plans provide the benefit of cashless treatment at a network of hospitals. This means that the insurer will directly settle the medical bills with the hospital, offering convenience and ease to the policyholder. This feature ensures that the policyholder does not have to bear the financial burden at the time of treatment, making the process smoother and hassle-free.

Tax Benefits - Premiums paid for family health insurance plans can be deducted from your taxes under Section 80D of the Income Tax Act, allowing you to save money on your tax liability. This means that you can lower your taxable income by the amount of health insurance premiums you've paid for your family.

Maternity Benefits - Some insurance plans provide comprehensive maternity benefits that cover pre and post-natal expenses, as well as medical care for the newborn. These benefits can include hospital stays, doctor visits, and other related costs, helping to ease the financial burden of having a baby.

Preventive Health Check-ups - Some insurance plans offer the benefit of free or discounted annual health check-ups for the insured family members. These preventive health check-ups are important for early detection of any potential health issues and can help in maintaining overall well-being.

Automatic Restoration of Sum Insured - Certain insurance plans provide automatic restoration of the sum insured if it is depleted within the policy duration. This guarantees that the family will have sufficient coverage throughout the entire year.

Long-Term Discounts - Opting for a multi-year family health insurance plan (2-3 years) can offer significant premium discounts, which can make it more budget-friendly over the long term. This approach allows you to lock in a lower rate for an extended period, providing financial stability and peace of mind for your family's healthcare needs.

Mid-term Inclusions - Insurers often offer mid-term inclusions, allowing policyholders to add new family members, such as a newborn baby or newly married spouse, by paying an additional premium.

Loyalty Discounts - Loyalty discounts are available for policyholders who keep their coverage for an extended period. These discounts aim to encourage long-term loyalty in customers by offering lower premiums upon renewal.

Pre-Existing Disease Buy-Back - The Pre-Existing Disease Buy-Back is a valuable optional cover that can significantly reduce the waiting period for pre-existing conditions. This means that individuals can benefit from quicker coverage and access to necessary medical treatments related to these conditions.

AYUSH Treatment Coverage - Hospitalization expenses for AYUSH treatments, including Ayurveda, Yoga, Unani, Siddha, and Homeopathy, are included in specific insurance plans. This coverage provides policyholders with the option to seek alternative forms of treatment and have the costs covered during hospitalization.

Which Factors Should You Keep in Mind While Selecting a Family Health Insurance Plan?

Choosing the best health insurance plan for your family can be overwhelming due to the wide variety available. To make the best choice, there are a few key factors to consider. These include -

Reviewing coverage benefits is crucial when buying a family health insurance. Policies cover inpatient care, pre/post-hospitalization costs, childcare, home care and ambulance expenses. Also, consider additional benefits like restoration lifetime sustainability, tax breaks etc.

Choose coverage for cashless claims at top city hospitals within the network of your insurance company. Ensure your chosen hospital is on the list for easy access to treatment.

All health insurance companies have the same claim settlement process, so it is important to check the claim settlement ratio of the company you are considering.

Compare the available plans in the market to understand them better.

Read the plan exclusions before buying to void confusion about services.

Check if your chosen plan covers your prescription drugs and note if there are any restrictions or formularies.

Evaluate your family's healthcare needs including family members, ages, pre-existing conditions, medical needs, medications, maternity coverage, pediatric care, specialist visits and ongoing treatments.

Conclusion

Securing a family health insurance plan is a crucial decision to protect your family's well-being amidst increasing medical expenses in India. It's important to analyze coverage options, network hospitals, claim settlement ratio, and long-term affordability to select a plan that suits your family's healthcare needs. Planning ahead and taking a proactive approach are key to ensuring your family's financial stability in case of a medical crisis.

Frequently Asked Questions (FAQs)

Q: Which is the best health insurance in India for families?

A: Some of the top family health insurance plans prioritize comprehensive coverage, high claim settlement ratios and competitive premium costs. Evaluating these factors is crucial for ensuring that the families receive the best possible healthcare protection.

Niva Bupa ReAssure 2.0: Claim Settlement Ratio (CSR) of 99.99%, coverage from ₹5 lakh to ₹1 crore.

Care Supreme: 100% CSR, coverage from ₹7 lakh to ₹1 crore.

ManipalCigna ProHealth Prime Advantage: CSR of 99.90%, coverage from ₹5 lakh to ₹1 crore.

Aditya Birla Activ Health Platinum Enhanced: CSR of 99.41%, coverage from ₹2 lakh to ₹2 crore.

Star Health Assure: CSR of 99.06%, coverage from ₹5 lakh to ₹2 crore.

Reliance General Health Infinity: CSR of 98.65%, coverage from ₹5 lakh to ₹5 crore

Q: How much does family health insurance cost in India?

A: Family health insurance costs can differ significantly due to factors like the age and health history of the insured members, as well as the chosen sum insured. Typically, a family of four can anticipate paying around 1,700 rupees to 2,200 rupees per month for a family floater with a coverage of 10 lakh rupees.

Q: What is a 5 lakh health insurance scheme?

A: The ₹5 lakh health insurance scheme or the Pradhan Mantri Jan Arogya Yojana (PMKAY) scheme offers coverage for medical expenses up to 5 lakh rupees, encompassing hospitalization treatments such as surgeries, room rents and other associated costs.

Q: What is the age limit for family insurance?

A: The age limit for dependent children in family health insurance plans is generally up to 25 years and for dependent parents is typically 65 years. It is important to note that different plans may have different criteria, so it is advisable to check the specific policy details.

Q: What is the waiting period for health insurance?

A: The waiting period in health insurance is an important aspect as it determines when you can claim benefits for certain conditions or treatments. It's crucial to carefully review the terms of your policy to understand the specific waiting periods that apply, as they can vary significantly depending on the type of illness or condition. Generally, waiting periods for general illnesses are around 30 days, but for pre-existing conditions, it could be as long as 2-4 years.

Q: How to claim family health insurance?

A: To claim family health insurance, you have to submit the necessary documents to the insurance provider, either directly or via the network hospital if you're choosing cashless claims. These documents usually consist of the health insurance policy, medical reports, ID proof, address proof, and any other documents required by the insurer. After reviewing the claim, the insurance company will settle it according to the terms and conditions of the policy.

Q: Can we add a family member to existing health insurance?

A: You can typically add family members to your health insurance mid-term, such as newly married spouses, newborn babies or adopted children, by paying an extra premium. Just keep in mind that there might be a waiting period for coverage of pre-existing conditions.

Q: Which company is best for family health insurance?

A: The best companies for family health insurance are Star Health, ICICI Lombard, and Tata AIG. These insurers offer comprehensive coverage, cashless hospitalization, maternity benefits, and automatic restoration of the sum insured. Consider factors like coverage, sum insured, network hospitals, claim settlement ratio, and premium affordability when choosing a family health insurance plan.

Q: Which health insurance is best for a middle-class family?

A: Consider opting for a family floater health insurance plan with a sum insured ranging from ₹5-10 lakhs, designed specifically for middle-class families. It should cover cashless hospitalization, pre and post-hospitalization expenses, daycare procedures, and AYUSH treatments. Verify that the premium is reasonable and provides eligibility for tax benefits under Section 80D of the Income Tax Act.

Q: Which is the best cashless health insurance in India?

A: Navi Health Insurance is highly recommended in India for its comprehensive coverage and wide range of network hospitals, making it a top choice for cashless health insurance.

Q: Is pregnancy covered by health insurance?

A: It's important to note that while many health insurance policies do provide coverage for pregnancy-related expenses and maternity benefits, the specific extent of coverage can vary widely. Therefore, it's crucial to carefully review the terms of your individual policy to understand what is included and what may not be covered.

Author: Abhik Das

Abhik Das is a versatile content writer with over 5 years of experience crafting engaging and informative content across diverse industries. His expertise spans the fields of ed-tech, pharmaceuticals, organic food, travel, sports, and finance.

Here's what sets Abhik apart:

Content Versatility: Able to adapt writing style and tone to suit various audiences and content needs.

SEO Proficiency: Creates content optimized for search engines, ensuring discoverability and organic traffic.

Deep Research: Conducts thorough research to ensure content accuracy and credibility across complex topics.

Engaging Storytelling: Captures reader interest with clear, concise, and compelling writing.

Abhik's diverse background empowers him to deliver insightful content across a wide range of subjects. Whether you're seeking engaging explainer pieces on the latest financial trends, informative guides to organic food choices, or captivating travelogues, Abhik has the expertise to craft content that resonates with your audience.