All Post

Top 8 Benefits of Recurring Deposit (RD) in India: Why It's a Smart Savings Option in 2026

Jul 10th 2026

Fixed Deposit

Every financial advisor will tell you to invest. But most people struggle with one simple problem: they never have a lump sum ready.Salary comes in. Rent goes out. Groceries, EMIs, school fees -...

Read more...

What Are Corporate FDs? Corporate FD vs Bank FD: Key Differences, Benefits & Risks (2026)

Jul 10th 2026

Fixed Deposit

Corporate fixed deposits are term deposits offered by companies and NBFCs to raise money from investors, while bank FDs are deposits accepted by banks from customers. Corporate FDs usually...

Read more...

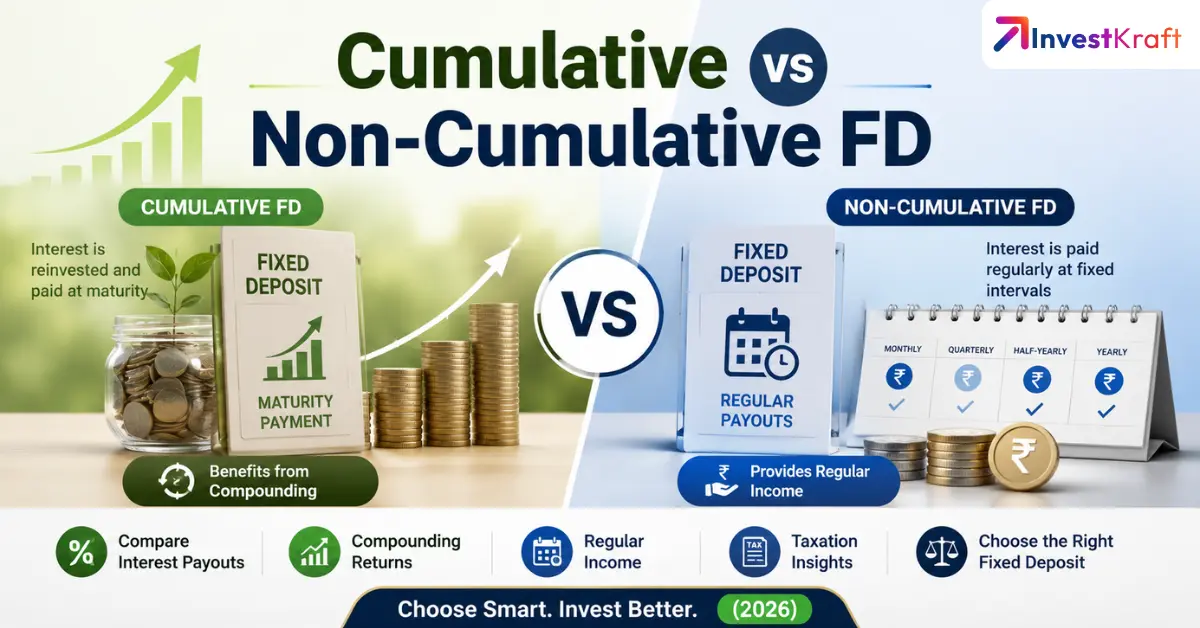

Cumulative vs Non-Cumulative FD: Key Differences, Returns & Which One to Choose (2026)

Jul 10th 2026

Fixed Deposit

Fixed deposits (FDs) are one of the most popular investment options in India, offering safety and predictable returns. However, many investors get confused when choosing between cumulative and n...

Read more...

Best FD Options for Senior Citizens in 2026: Compare Highest Interest Rates, SCSS & Bank Fixed Deposits

Jul 2nd 2026

Fixed Deposit

If you are a senior citizen and planning to do a fixed deposit, then you can earn anywhere from 7% to 8.75% per annum on a government-regulated, fully insured fixed deposit - that's a meaningful incom...

Read more...

7 Strategies for Breaking Fixed Deposit (FD) Without Penalty Charges in 2026

Jul 2nd 2026

Fixed Deposit

If you have a sudden and unexpected expense, and are planning to break your FD prematurely, then we would strongly recommend holding that thought there and giving this article a read, as this might sa...

Read more...

Foreign Banks in India: Complete List, Top International Banks, Benefits & How They Operate (2026 Guide)

Jun 29th 2026

Finance

Foreign banks have become an important part of India's banking ecosystem, offering world-class financial services to multinational companies, institutional investors, high-net-worth individuals...

Read more...

Best Websites to Make Money Online in India (2026): 20 Trusted Platforms to Earn Without Investment

Jun 27th 2026

Finance

Whether you're a student looking for a side hustle, a working professional wanting an additional income stream, a homemaker searching for flexible work-from-home opportunities, or a freelancer a...

Read more...

Personal Loan for Women in India 2026: Eligibility, Interest Rates, Government Schemes & Options for Housewives

Jun 27th 2026

Personal Loan

Two women apply for the same ₹5 lakh personal loan. One is a working professional with a salary slip. The other is a homemaker with no formal income - but she manages the household budget, has g...

Read more...

Types of Fixed Deposits in India (2026): Best FD Options to Maximise Returns

Jun 26th 2026

Fixed Deposit

Fixed Deposits (FDs) remain the bedrock of Indian household savings. Despite the rise of mutual funds, stock markets, and crypto, the humble FD continues to attract crores of investors - and for...

Read more...

Best Fixed Deposit Interest Rates in India 2026: Compare PSU, Private and Small Finance Banks

Jun 26th 2026

Finance

If you have money sitting idle in a savings account earning 2.5%-4% interest, a Fixed Deposit (FD) remains one of the simplest and safest ways to earn better returns without taking exposure to s...

Read more...

Latest Post

.webp)

Reach out to our Experts if you have any Doubts

Like the best things in life, Consultations @InvestKraft are free

Drop a Mail or give us a Missed Call & Begin your Investment Journey here